Information and materials on this page are

based on those provided by the author, Dr. Belay Seyoum

Chapter Outline

Background

Exporters prefer to be paid on or

before shipment of the goods, whereas buyers want to delay

payment until they have sold the merchandise.

To expand export sales, many

governments offer a wide choice of financing programs.

Such assistance increases the

exporter's credit line needed for corporate and domestic

transactions, neutralizes financing as a factor, and creates a

level playing field with competitors in other countries who also

benefit from similar financing programs.

The OECD (Organization for

Economic Cooperation and Development) has developed guidelines

on export credits for its members.

Chapter 01.

Growth and Direction of International Trade

Chapter 02. International and Regional Agreements

Affecting Trade

Chapter 03. Setting Up

the Business

Chapter 04. Planning

and Preparations for Export

Chapter 05. Export

Channels of Distribution

Chapter 06.

International Logistics, Risk, and Insurance

Tariffs and Nontariff Barriers as Import Restrictions

Methods of Levying Tariffs

1.

Ad valorem:

Duty based on value of the imported

product

2.

Specific:

Duty based on quantity or volume

3.

Compound:

Duty that combines both ad valorem and

specific

Nontariff Barriers

Nontariff barriers include quotas, tariff quotas, labeling

requirements, licensing

requirements, prohibiting the entry of certain imports, and

requirements

to purchase domestically produced goods.

Preferential Trading Arrangements

NAFTA, U.S./Israel FTA, U.S./Australia FTA, the Caribbean Basin

Initiative,

Andean Trade Preference, the Generalized System of Preferences,

AGOA.

Trade Intermediaries and Services

Customs brokers, free-trade zones, and bonded warehouses.

Customs Brokers

Customs brokers act as agents for importers with regard to (1)

the entry

and admissibility of merchandise, (2) its classification and

valuation, and

(3) the payment of duties and other charges assessed by customs

or the refund

or drawback thereof.

Export-Import Bank of the United States (Eximbank)

Eximbank

is an independent agency of the U.S. government, the purpose of which is

to aid in financing and to facilitate trade between the United States

and other countries.

The

bank, which is expected to be self–sustaining (except for the initial

capital of $1 billion to start operations), makes loans and guarantees

with reasonable assurance of repayment. It complements private sources

of finance.

Major Export Financing

Programs Provided by Eximbank

Working Capital Guarantee

Program

This

enables exporters to meet critical pre–export financing needs, such

as inventory build up or marketing. Eximbank will guarantee 90

percent of the loan provided by a qualified lender. The guarantee

has a maturity of twelve months and is renewable.

The

major features of the working capital guarantee program are as

follows:

Qualified

Exports: Eligible

exports must be shipped from the United States and have at least

50 percent U.S. content.

Guarantee Coverage and Term of

the Loan: In

the event of default by the exporter, Eximbank will cover 90

percent of the principal of the loan and interest, up to the

date of claim for payment, insofar as the lender has met all the

terms and conditions of the guarantee agreement.

Collateral and Borrowing

Capacity:

Guaranteed loans are to be secured by a collateral.

Qualified Exporters and Lenders:

Exporters must be domiciled in the United States (regardless of

domestic/foreign ownership requirements), show a successful

track record of past performance, including an operating history

of at least one year, and have a positive net worth.

Export Credit Insurance Program

A

wide range of policies to accommodate different insurance needs. Its

major features are: U.S. content requirements, restrictions on sales

destined for military use and to communist nations.

Short–term single–buyer policies: These cover a single sale

or repetitive sales over a one–year period to a single buyer.

They provide coverage against political and commercial risks.

They support products such as consumables, raw materials, spare

parts, low–cost capital goods, etc.

Short–term multibuyer policies: These cover short–term

export sales to many different buyers against political and

commercial risks. Product coverage is the same as above.

Small

business policy (graduate to short–term multibuyer when

annual export credit sales exceed $3 million): This short–term

policy covers small businesses with average annual export credit

sales of less than $3 million. It provides coverage against

political and commercial risks.

Small

business environmental policy: This short–term policy

provides coverage to small businesses that export environmental

goods and services against political and commercial risks.

Financial institution buyer credit policy: This protects

financial institutions against losses on short–term direct

credit loans or reimbursement loans to foreign buyers of U.S.

goods and services.

The

bank letter of credit policy: This provides coverage against

the failure of a foreign financial institution (the issuing

bank) to honor its letter of credit to the insured bank.

Financing and operating lease policy: These two separate

leases provide coverage against political and/or commercial

risks—policies protect lessor against loss of a stream of lease

payments and fair market value of the leased product.

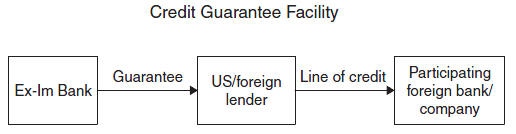

Guarantees:

The program provides repayment protection for private–sector loans

to creditworthy buyers of U.S. goods and services. There is also

special coverage for U.S. or foreign lenders on lines of credit

extended to foreign banks or foreign buyers.

Direct

Loan Program:

This is an intermediate/long–term loan provided to creditworthy

foreign buyers for the purchase of U.S. capital goods and services.

Project Finance Program:

This program supports exports of U.S. capital equipment and related

services for projects whose repayment depends on project cash flows,

as defined in the contract.